My name is Lewis Sterriker. I am an equity research analyst at Marvin Labs, covering the gaming sector and its adjacent industries. About fifteen years ago I was a professional gamer, which is either the most useful or the most distracting background an analyst covering this space could have, depending on who you ask.

I mention this because it shapes the way I work. When I read a quarterly filing from EA or Ubisoft, I am not reading it cold. I have context from years spent inside the products these companies sell, and that context influences where I look for information and which sources I take seriously. It introduces biases I have to manage. But it also means I know when a company is describing its own game inaccurately, and that is worth something.

This piece is about the sources I use when writing investment primers, thematic pieces, and reactive commentary on gaming companies, and how I think about which ones deserve weight. I am describing my process, not prescribing yours.

The Chain

I think of sources as a chain ordered by veracity. The higher up the chain, the more confidence I have in using that source to underpin a thesis or support a claim in a published piece.

And no, this is not inspired by Andrew Ryan's Great Chain, or the Chain of Balance from OG God of War. Come to think of it though, the latter might be fun to play with.

The Chain of Balance connects Olympus to the Underworld. It holds the cosmology together. Sever it and both realms collapse. The source chain in equity research is not quite that dramatic, but the architecture is similar: at the top sit the sources that carry the authority of legal obligation, structured disclosure, and regulatory scrutiny. At the bottom sit the sources that are fast, unfiltered, and occasionally brilliant, but carry no such weight. The chain holds because each tier has a function. Cut any section out entirely and the work suffers for it.

The upper reaches are Olympus. The lower reaches are the Underworld. Both are necessary. The difference is in how much armour you need to wear when you walk through them.

From Olympus

| Tier | What it gives you | Where it stops |

|---|---|---|

| Primary filings (10-K, 10-Q, proxy, transcripts, investor presentations) | Management on the record, under legal obligation. Structured, citable, auditable. | Distortion by emphasis. Disclosure gaps are deliberate. |

| Verification platforms (Bloomberg, WSJ, Yahoo Finance) | Cross-referencing metrics against your own models. | Platforms disagree with each other. Lookback windows and calculation methods vary. |

At the top sit primary filings. They are not free of distortion — management teams emphasise what flatters and contextualise what does not — but the distortion is structured, and a careful reader learns to account for it. If you are coming from a sector where management commentary tends to be more guarded than it is in gaming, you may find the candour surprisingly useful. Andrew Wilson at EA will describe individual gameplay mechanics in an earnings call. Shuntaro Furukawa at Nintendo will talk about hardware design philosophy. That granularity is a gift. Use it.

Below that sits the verification tier. I do not take platforms like Bloomberg or Yahoo Finance at face value. When I build a reverse DCF or calculate WACC, the model is constructed from the filings directly, and I trust my own work unless it is woefully distant from what multiple platforms report. Beta on Yahoo Finance and beta on Bloomberg for the same company on the same day can differ meaningfully depending on the lookback window and benchmark index. Building it yourself and then checking is a different discipline from looking it up and accepting it. I think the former produces better analysts.

These two tiers are where primers live and breathe. When I built the AMD primer, every revenue segmentation figure, every data centre versus gaming mix breakdown, every margin trajectory was sourced from AMD's own 10-K filings and earnings transcripts. Lisa Su's commentary on EPYC adoption and Ryzen market share is specific enough to build models on, and that specificity is what makes it citable. If a data point does not come from a primary source, it does not appear in a primer. That is the cost of the format and the reason it carries the weight it does.

This is Olympus. The air is thin, the sources are auditable, and the prose is written to survive scrutiny.

Into the Underworld

Below the verification tier, the chain descends. The sources become faster, more granular, and more interesting, but less structured and less accountable. This is where an analyst covering gaming diverges most sharply from one covering industrials or consumer staples.

Consider what follows a guided descent. The sources cited below are landmarks I have found useful, offered in the same spirit a ferryman might point out the rocks. What you make of them is your own affair.

| Tier | What it gives you | Where it stops |

|---|---|---|

| Elysium — Industry data (Steam Charts, Circana, SensorTower) | Real-time performance data at a granularity filings cannot match. | Platform-specific coverage. Inference required for cross-platform conclusions. |

| Asphodel — Journalism (Bloomberg, Forbes, Kotaku, Polygon, IGN) | Studio culture, development timelines, internal morale. | Different evidentiary standards. A well-sourced article is a lead, not a confirmable fact. |

| The River Styx — Social and video (YouTube, X, Bluesky, Reddit, Discord) | Speed, community sentiment, early signals. | Unverified by default. Credibility follows the person, not the platform. |

Elysium — Industry-specific data

If the Underworld has a pleasant district, this is it. The data here is real, sourced, and often granular enough to be genuinely useful. The limitation is not quality but coverage.

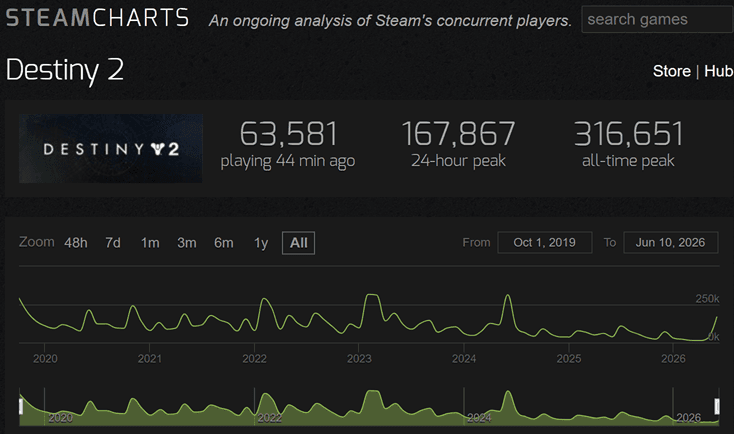

Steam Charts tracks concurrent player counts on Valve's PC platform. What it will not tell you is how a game performs on PlayStation, Xbox, or Nintendo hardware — there is no publicly available equivalent. The inference that Steam numbers serve as a bellwether for broader platform performance is common and not unreasonable, but it is an inference, not a measurement, and the distinction matters when building a thesis on it.

What matters is knowing what you are looking at. Almost every game launches with a spike that reflects marketing spend and curiosity as much as product quality. That peak is noise. The stabilisation floor — the level at which concurrent users settle once the launch window closes — is the signal. If that floor holds, you have a basis for projecting sustained engagement. If the curve decays sharply and does not stabilise, the live-service thesis is in trouble regardless of launch numbers.

Destiny 2 shows the pattern in decline. The Final Shape expansion spiked the all-time peak to 316,651 in June 2024, but the curve never stabilised — decaying through 100k, 77k, 59k across successive quarters. By Q1 2026, peak concurrents had fallen below 30,000. That told you the franchise was in structural trouble well before the shutdown announcement in May 2026.

Then there is Circana, and specifically Matt Piscatella. His data on US consumer spending, hardware sell-through, and market trends is syndicated, sourced, and cited across the industry. He occupies a rare position at this tier: a source whose credibility approaches what you would expect a tier higher. When Piscatella posts weekly engagement rankings or hardware sales data, it is sourced market research with institutional accountability behind it.

SensorTower does something similar for mobile. If you are covering a publisher with meaningful mobile exposure — Take-Two through Zynga, EA through its mobile sports titles — SensorTower gives you a cross-reference point that filings alone cannot. The same caveats apply: estimated data, not disclosed.

Asphodel — Journalism

Asphodel is where the ordinary dead go. Not punished, not rewarded. Just there. Games journalism earns the label: it contains both genuine investigative work and a considerable volume of material that prioritises ideological framing over business or craft analysis. Separating the two is the discipline this tier demands.

The best of it surfaces information filings will never contain. Jason Schreier at Bloomberg has been consistently ahead of filings on studio culture, project cancellations, and internal decision-making at major publishers. His reporting on Bungie's layoffs following the end of Destiny 2 development laid the groundwork for the shutdown story long before any earnings call acknowledged the scale of the problem. Paul Tassi at Forbes occupies a different lane: more prolific, more reactive, closer to the daily rhythm of the community. Both have track records that make their work worth incorporating into thematic pieces and reactive commentary, where the evidentiary bar is different from a primer.

Sites like Kotaku, Polygon, and IGN sit lower within Asphodel. A Kotaku investigation into crunch at a major studio can be valuable. A Kotaku opinion piece on whether a character design is politically appropriate cannot. The sites produce both, often on the same day, and the ratio is not always in your favour.

The distinction between journalism and the filing-driven work at the top of the chain is a hierarchy of verifiability, not quality. A Schreier article about internal turmoil at a studio is often more informative than the quarterly filing that studiously avoids mentioning it. But "informative" and "citable in a primer" are not the same thing, and the analyst who conflates them will eventually get burned.

The River Styx — Social and video commentary

Noise is the governing condition of this tier. If the signal versus noise framing from the Project Genie sell-off piece applies anywhere on this chain with full force, it is here.

The journalistic tier and this one converge more than the hierarchy implies. Schreier has a YouTube channel. When he publishes a video discussing the same story he reported on in print, the source credibility does not change because the medium did.

Then there are channels that sit purely in the video space but operate with rigour. Bellular News produces daily coverage with strong citations and perspectives that are genuinely their own. Skill Up is thorough and well-researched, though his coverage can lean editorial in ways that serve his audience more than they serve an analyst. Once you have watched enough of these channels to trust their editorial standards, they become part of your regular intake.

Personal taste becomes unavoidable here. I gravitate toward Bellular over YongYea or Legendary Drops. That is not a judgment on quality. It is a statement about what I find useful.

Bluesky, X, and the data layer. Piscatella is also active on Bluesky and X, where the same institutional data he publishes through Circana reaches a wider audience on platforms otherwise dominated by opinion. Daniel Ahmad operates similarly on X, covering global market data and hardware trends with a regional depth that English-language coverage often misses.

Reddit and the black market. Reddit is the Tartarus of the chain, and I mean that as something closer to a compliment than it sounds. It is where the most unfiltered, most operationally specific information about how games actually work tends to surface.

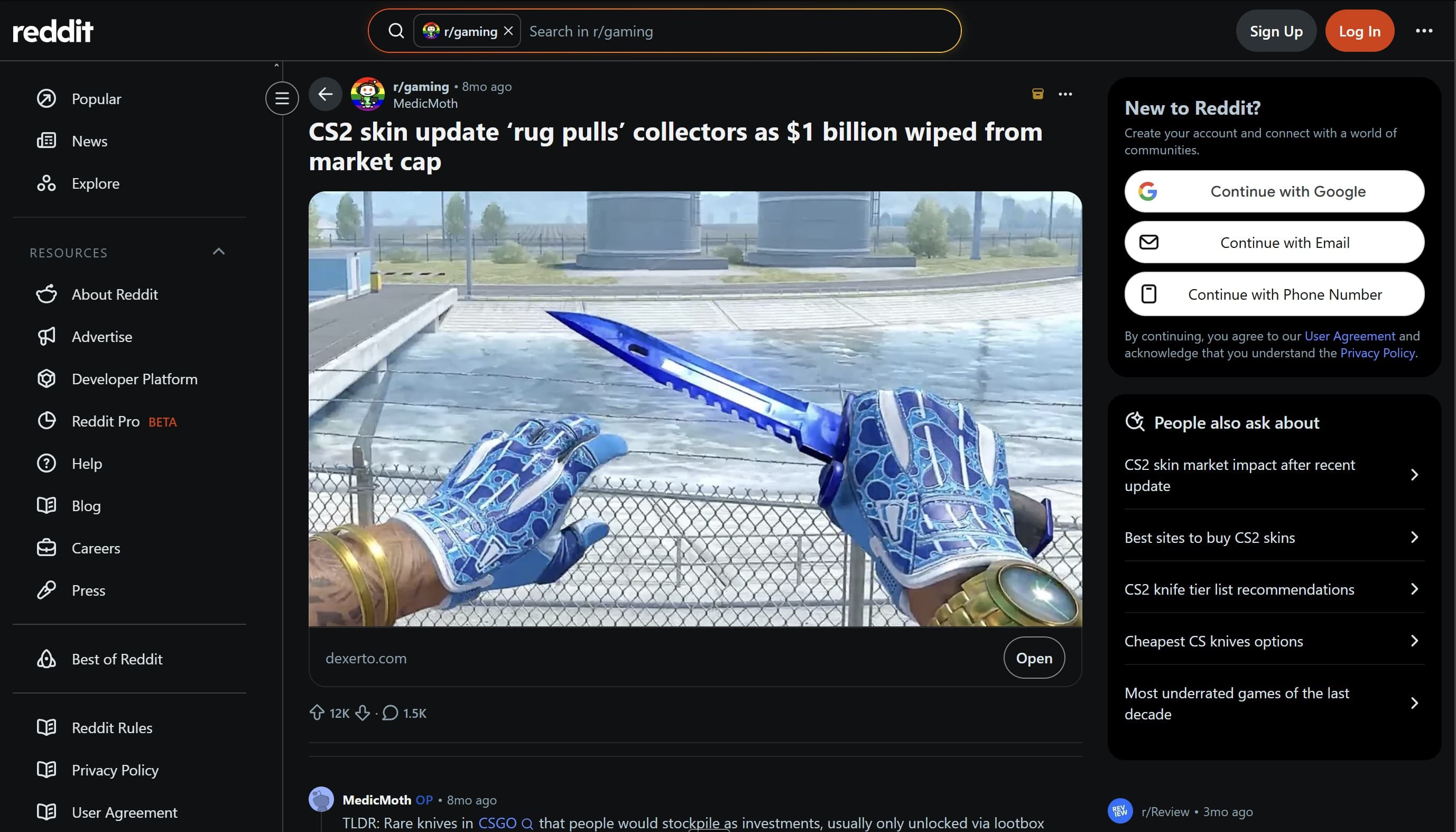

When I was researching Valve's skins economy, Reddit was the primary venue for understanding the mechanics at ground level: how skins are priced, traded, and valued, how third-party marketplaces interact with Steam's ecosystem, and where the grey areas sit. Valve is private and discloses nothing. The Reddit threads were not the source. They were the map to the source. When a Counter-Strike 2 skin update wiped $1 billion from the secondary market, it was Reddit that documented the mechanics and the fallout in real time — the kind of granularity that no filing will ever provide, because no filing needs to.

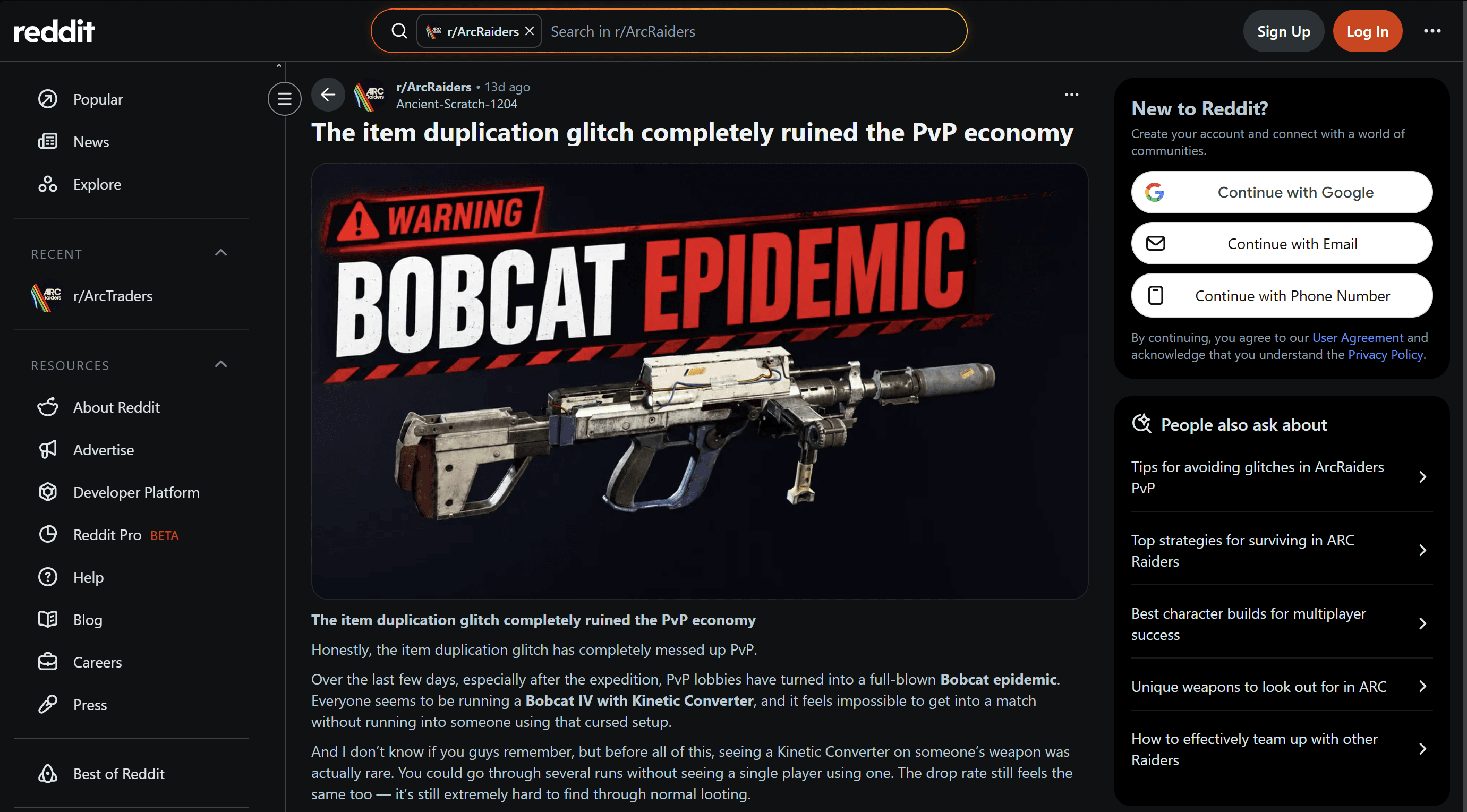

The same pattern applies to real-time intelligence on exploits. The Arc Raiders weapon duplication glitch is a current example: a bug that allowed high-tier weapons to be duplicated at scale, undermining the game's entire PvP economy. That story surfaced on Reddit before anywhere else.

For an analyst covering the publisher, knowing about these things early is the difference between asking an informed question on the next earnings call and reading about it after the fact.

Discord. Discord is less a source and more a venue for prospecting: overhearing conversations in gated communities where developers, journalists, and engaged players talk with a candour no public platform permits. It is where leads for thematic and reactive pieces originate. That is its value. That is the extent of its value. Discord conversations are ephemeral, ungated in the wrong direction, and impossible to cite. Using Discord intelligence in serious analytical work would contaminate it.

A claim made in a YouTube video, a Reddit thread, or a Discord channel is not a source. It is a lead. You follow the citations until you arrive at something you can verify independently, or until you hit a wall. Sometimes the trail leads back to Olympus. Sometimes it dead-ends at another opinion, and the observation stays in your notes rather than your draft.

Narrative capture

The Underworld tests a discipline that is worth naming on its own, because the failure mode is subtle and the consequences compound.

Studio-level reporting can generate strong reactions that have no proportionate impact on the equity. The shutting down of Destiny 2 is the clearest recent example. The reporting paints a picture of mismanagement, cultural dysfunction, and a studio that lost its way after independence. Read enough of it and you will come away convinced that Bungie is a disaster. And Bungie may well be a disaster. But how bad is it for Sony?

Based on the work I have done on this question ahead of a piece on the shutdown, Sony's Games & Network Services segment posted record operating income in FY2025 despite absorbing two separate Bungie impairment charges totalling over $765 million. Strip those charges out and the segment's underlying operating margin was approaching 13%. The acquisition looks badly judged. The company does not look like one in crisis.

This is narrative capture: the moment a studio-level story, amplified by journalism and social media, starts driving your view of the parent equity without passing through the filings first. The Underworld will tell you Bungie is in crisis mode. The community reaction, vice and virtue both present and correct, is static. Olympus will tell you Sony can absorb it. Knowing which question you are actually trying to answer, and which tier is equipped to answer it, is the entire point of this chain. The lower you go, the more vivid and emotionally compelling the narratives become. That vividness is the risk. An analyst who lets it override what the filings say has lost the thread.

How the format changes which tiers I use

The type of piece determines how far down the chain I go.

For investment primers, the chain stops at Olympus. A primer articulates what must be true for a thesis to hold, and every claim needs to stand on ground that cannot be disputed as a matter of record.

For thematic pieces and reactive commentary, the entire chain is available. The EA piece on the $55 billion leveraged buyout draws on filings and transcripts, but the framing was informed by months of watching the community response across forums, YouTube, and X. A thematic piece might begin with something I noticed at the base of the chain and traced upward until I either reached a primary source or the trail went cold. The tracing is the work.

The quant side

Quantitative data presents a simpler chain but a faster floor.

Financial modelling draws almost exclusively from company filings. When I build a reverse DCF for a primer, like the ones underpinning the Apple and Constellation Energy pieces, every assumption is derived from the numbers management provides. There is no shortcut here and there should not be one.

Where the floor arrives quickly is in disclosure gaps. Apple does not break down its Services revenue by component. Netflix has pulled back from disclosing retention data and total subscriber numbers. When the granularity you need simply does not exist in the filings, you are left with inference, and inference built on absent data is a fundamentally different thing from analysis built on present data. The honest response is to name the gap and let the reader make their own judgment.

If you are coming from a sector with more prescriptive disclosure requirements, gaming will frustrate you. Unit volumes are rarely disclosed. Per-title revenue breakdowns are almost never available. This is not a solvable problem. It is a condition of the coverage.

When the top of the chain goes quiet

When management withholds a metric, or restructures reporting segments in ways that obscure what was previously visible, the top of the chain goes silent on the specific thing you need. If the missing metric is load-bearing for your thesis, you have to look elsewhere.

This is where the lower tiers become compensatory. A live-service game's Steam retention curve, Twitch viewership trends, community sentiment tracked across Reddit and Discord: none of these substitute for what a company could tell you in a filing. But when the company chooses not to, they are sometimes the only signal available.

Consider a publisher that stops disclosing monthly active users for a flagship title after several quarters of decline. The filing will still report segment revenue, and you can work backwards to infer engagement trends. But the inference gets looser the more revenue streams are bundled into the same segment. If you want to understand whether the player base is stabilising, contracting, or migrating to a competitor, you will find more signal in the subreddit activity, in the Twitch viewership data, than in anything the quarterly filing is willing to give you.

The important thing is to be explicit about what you are doing. This is using the lower tiers because the top of the chain has failed you on a specific question. Sometimes the compensatory signal is strong enough. Sometimes it is not, and you say so. The honesty about the substitution is what separates analysis from speculation.

LLMs in the chain

I use large language models in my research, and I do not think there is anything to be squeamish about in saying so.

I do not use LLMs to generate analysis or to produce text I pass off as my own thinking. I use them to find information, to verify claims across sources, and as interlocutors — something to think against when testing whether an argument holds together.

My practice is to use at least three different models for any significant verification task. If three independent models converge on the same factual claim and can point me toward the same primary sources, I have more confidence than if I had relied on one. I request citations. I follow those citations. I read the sources myself. The LLM is a search tool with conversational capabilities, not an oracle.

Marvin Labs builds a platform that makes the primary-source gathering phase substantially faster: structured extraction from filings, earnings transcripts, and regulatory documents at a speed and consistency that manual search cannot match. It does not replace the analytical work. It accelerates the phase that precedes it.

The starter chain

If you are covering gaming for the first time, the full chain can wait. These are the sources I would tell a new analyst to follow before anything else:

| Source | Tier | Why |

|---|---|---|

| SEC EDGAR | Olympus | The filings themselves. Start here. Stay here longer than you think you need to. |

| Steam Charts | Elysium | Real-time engagement data for PC titles. Learn to read the retention curve, not the launch spike. |

| Matt Piscatella (Circana) | Elysium / Styx | Syndicated US market data with institutional credibility. His Bluesky feed is one of the few at that tier worth following daily. |

| Jason Schreier (Bloomberg) | Asphodel | The standard for investigative games journalism. His reporting on studio culture has been consistently ahead of filings. |

| Daniel Ahmad | Styx | Global market data, hardware trends, and regional context that English-language coverage often misses. |

These five will not give you everything. They will give you enough to know where the gaps are and which direction to look.

Where the chain ends

The sources are not the insight. The chain gives you discipline — a way to order what you encounter by how much confidence it deserves — but the judgment about where to stop, what to trust, and what to leave on the table is not something a hierarchy can provide. That is learned by doing the work, getting it wrong occasionally, and paying attention to which sources held up when the thesis was tested and which ones quietly fell apart.

I do not think my process is the right one for every analyst. I think it is the right one for the work I do, covering a sector where a concurrent player count on Steam and a footnote in a 10-K can both matter, depending on what you are trying to say and how much you need it to hold. If you are covering gaming for the first time, or covering it from a distance as many analysts do, I hope this gives you a sense of where the data lives. What you do with it is your own responsibility.